You run a clean business. You have happy buyers. You follow all the rules. So, why do banks keep rejecting your applications?

You are likely asking yourself: why am I high risk for payment processors? It feels incredibly unfair. I completely understand your frustration. You work hard to build your brand. But the rules of the game have changed drastically. Banks do not look at your business the way you do.

Let’s break down the real reasons behind your high risk status.

It Is Not About Your Chargebacks (Anymore)

Years ago, the high risk label made perfect sense. It meant your business had too much fraud. It meant you had too many unhappy customers asking for refunds.

That is not the case today.

Visa and Mastercard changed the entire global system. They now use Merchant Category Codes (MCCs). They tag every single industry with a specific code.

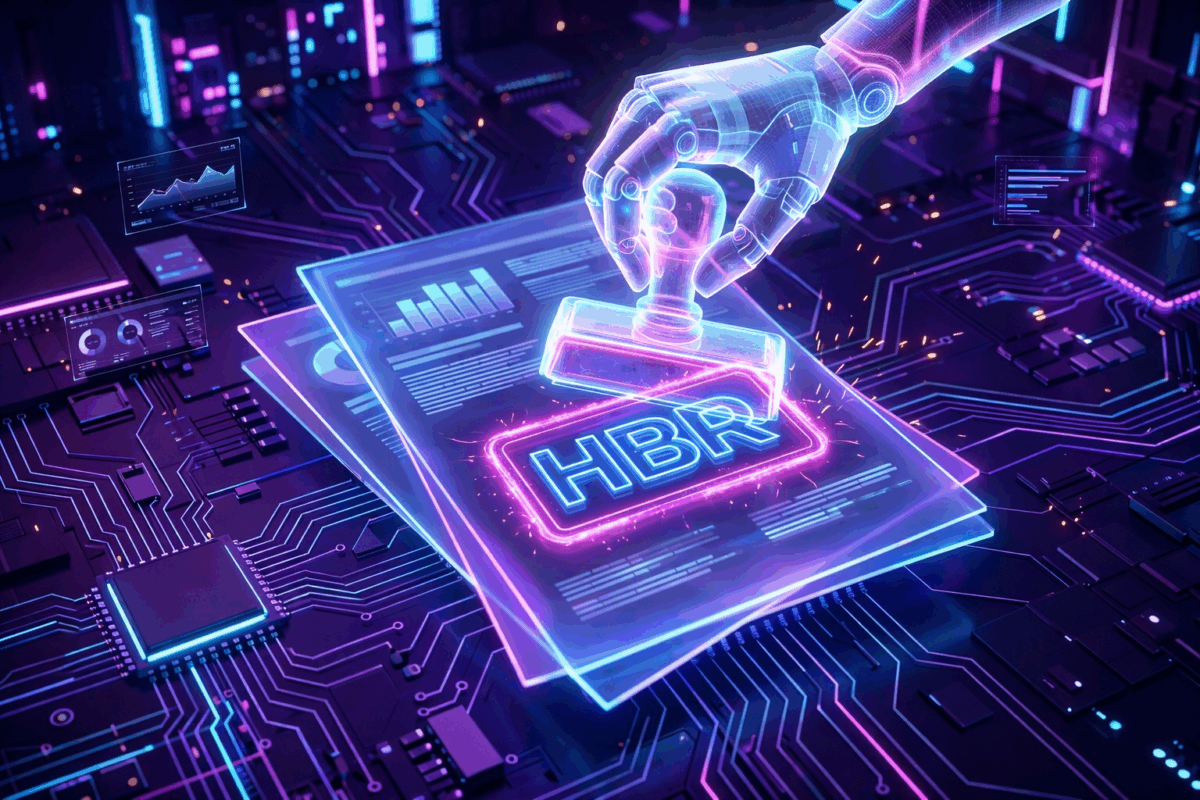

They also built a very strict list. It is called the HBR list. This stands for High Brand Risk. If your industry code is on the HBR list, you are automatically flagged. Your actual sales numbers and perfect history do not matter at all.

What Industries Are on the HBR List?

The HBR list covers many major markets. Here are a few common ones:

Adult content and entertainment.

Online gambling and sports betting.

Forex trading and crypto brokers.

Direct sales and telemarketing.

The Reputational Danger (Why Clean Businesses Get Flagged)

But wait. What if your industry is not on the HBR list at all? You might still find yourself needing a high risk merchant account.

Why does this happen? The answer is purely reputational risk. Banks absolutely hate bad press. They fear public scandals more than anything else.

For example, think about industries like CBD or AI generation websites. They are often classed as «medium/high risk.» With CBD, banks fear the lingering stigma around cannabis. With AI, they worry the software might generate prohibited content.

You might have perfect lab tests. You might have flawless code. You might despise illegal activities. It simply does not matter. The bank is just shielding itself from a potential PR disaster.

Stop fighting with traditional banks. You need a partner that understands your industry. Start processing payments for your high risk company NOW. You pay nothing unless approved. Reach out to the Ireowo team today.

So, Do Chargebacks Even Matter Now?

Yes. In fact, they matter more than ever before.

In the past, getting a high risk merchant account gave you breathing room. Some processors allowed up to 5% in chargebacks. Later, more conservative banks dropped that allowance to 2%.

Now? Almost all high risk processors have practically zero tolerance for fraud. This includes «friendly fraud,» where a real buyer falsely claims they did not buy the item.

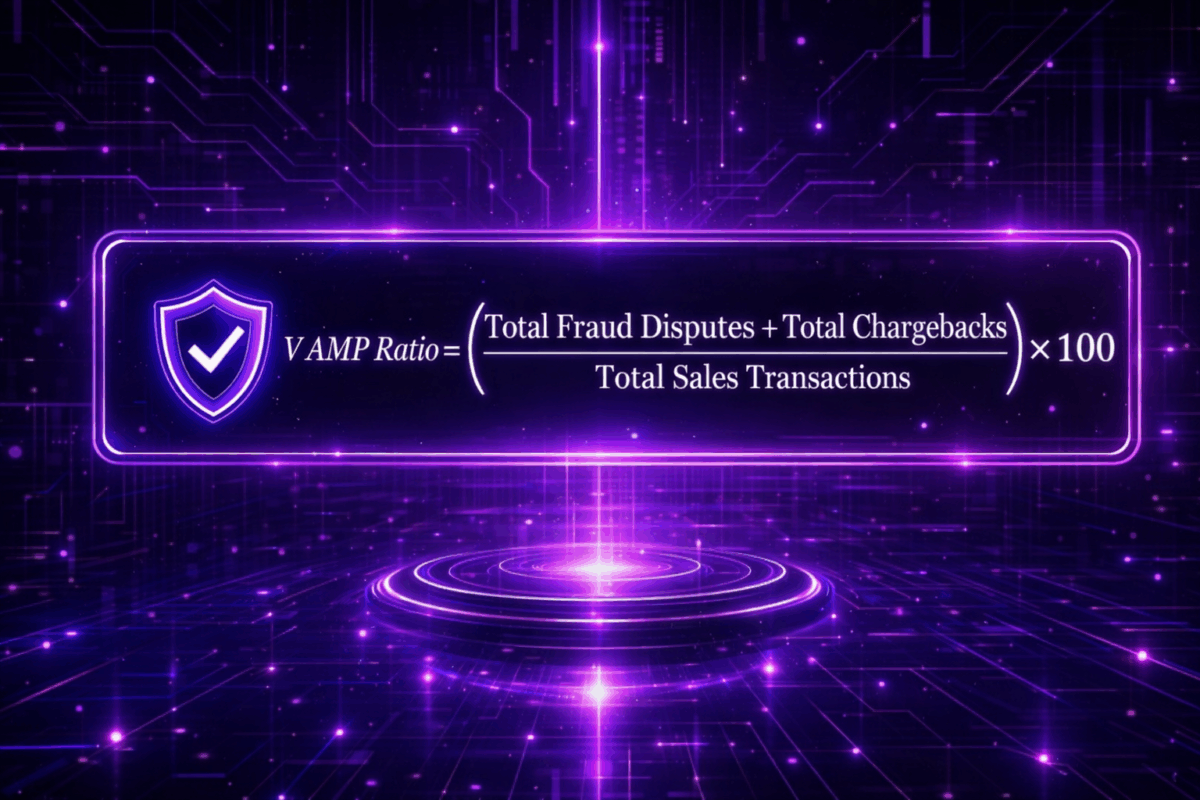

This massive shift happened because of VAMP. VAMP stands for the Visa Acquirer Monitoring Program. It forces processors to crack down on you instantly.

How Does VAMP Work?

The VAMP Ratio is calculated by dividing the total number of fraud disputes and chargebacks by the total number of sales transactions within the same month.

This formula is more stringent than previous iterations because it aggregates both fraud and chargebacks, preventing merchants from masking security issues under the guise of service disputes.

You can read the exact current thresholds directly on the Visa Core Rules and Product Rules official document.

The Hidden Threat: Automated Bank Flags

Here is a terrifying fact for business owners. In 80% of cases, your actual customers are not the ones reporting the fraud.

The buyers’ banks use highly aggressive automated systems. These bots scan transactions in milliseconds. They decide to flag your sales as «possible fraud» without any human input. This takes the control completely out of your hands.

There are smart anti-fraud systems to fight this. But they are not 100% infallible. Sometimes, they block perfectly good sales.

So, you face a brutal choice. What do you prefer?

Do you lose 10% of your sales to strict anti-fraud filters? Or do you risk your entire company being fined up to €50,000 by the card schemes?

Worse, if you ignore this, they will add you to the MATCH list. This is a global financial blacklist. If you land on it, getting a high risk merchant account becomes almost impossible. You can learn exactly how this blacklist operates by reading the official Mastercard MATCH system guide.

Do not risk massive fines or losing your business. Secure your checkout and start processing payments for your high risk company NOW. You pay nothing unless approved. Register with Ireowo today.

Curious Things You're Probably Wondering

01 Will the police seize my funds if my processor drops me?

No. This is a very common fear. If a bank closes your high risk merchant account, they do not call the authorities. They will simply freeze your funds for up to 180 days. This is just to cover any late chargebacks from your past buyers.

02 Can banks spy on my website to see what I sell?

Yes, they absolutely do. Payment processors use web scrapers continuously. These bots read your site daily. If they find prohibited words, medical claims, or banned ingredients, they will freeze your account in seconds.

03 Does my personal credit score drop if my store gets blacklisted?

Being placed on the MATCH list hurts your business deeply. However, it does not directly lower your personal credit score. But beware: opening any new business bank accounts or finding a new high risk merchant account will become a nightmare.