Introduction to KYC and Its Importance in Merchant Onboarding

In today’s digital financial ecosystem, Know Your Customer (KYC) isn’t just a compliance checkbox — it’s the foundation of trust, transparency, and security in merchant onboarding. For merchant account providers, implementing robust KYC onboarding practices helps prevent fraud, ensure regulatory compliance, and build long-term relationships with legitimate merchants.

With evolving anti-money laundering (AML) laws and stricter financial regulations, businesses that neglect KYC risk hefty fines, reputational damage, and account suspensions. Let’s explore how merchant service providers can master the art and science of KYC onboarding in 2025.

What is KYC (Know Your Customer)?

KYC is the process by which financial institutions and merchant service providers verify the identity of their clients. This verification ensures that businesses are legitimate and not engaged in illicit activities such as money laundering or fraud. The process typically involves collecting and validating identity documents, business licenses, and financial records.

Why KYC is Crucial for Merchant Account Providers

Merchant account providers operate at the intersection of payments and risk. They’re responsible for onboarding merchants who will process high volumes of transactions — making them prime targets for financial criminals.

Without strong KYC controls, providers can unknowingly facilitate fraudulent activities. Thus, effective KYC onboarding acts as a defensive shield that safeguards both merchants and the payment ecosystem.

The Role of KYC in Preventing Financial Crimes

Combating Fraud, Money Laundering, and Identity Theft

KYC helps detect unusual patterns early — whether it’s synthetic identity fraud or shell companies hiding illegal funds. By verifying ownership structures and beneficial owners, providers reduce exposure to criminal schemes.

Regulatory Frameworks Governing KYC Compliance

Merchant account providers must comply with standards set by global bodies like the Financial Action Task Force (FATF) and local regulators such as FinCEN (U.S.) and the European Union’s AML Directives (AMLD). Each framework outlines due diligence procedures to ensure consistent and lawful onboarding.

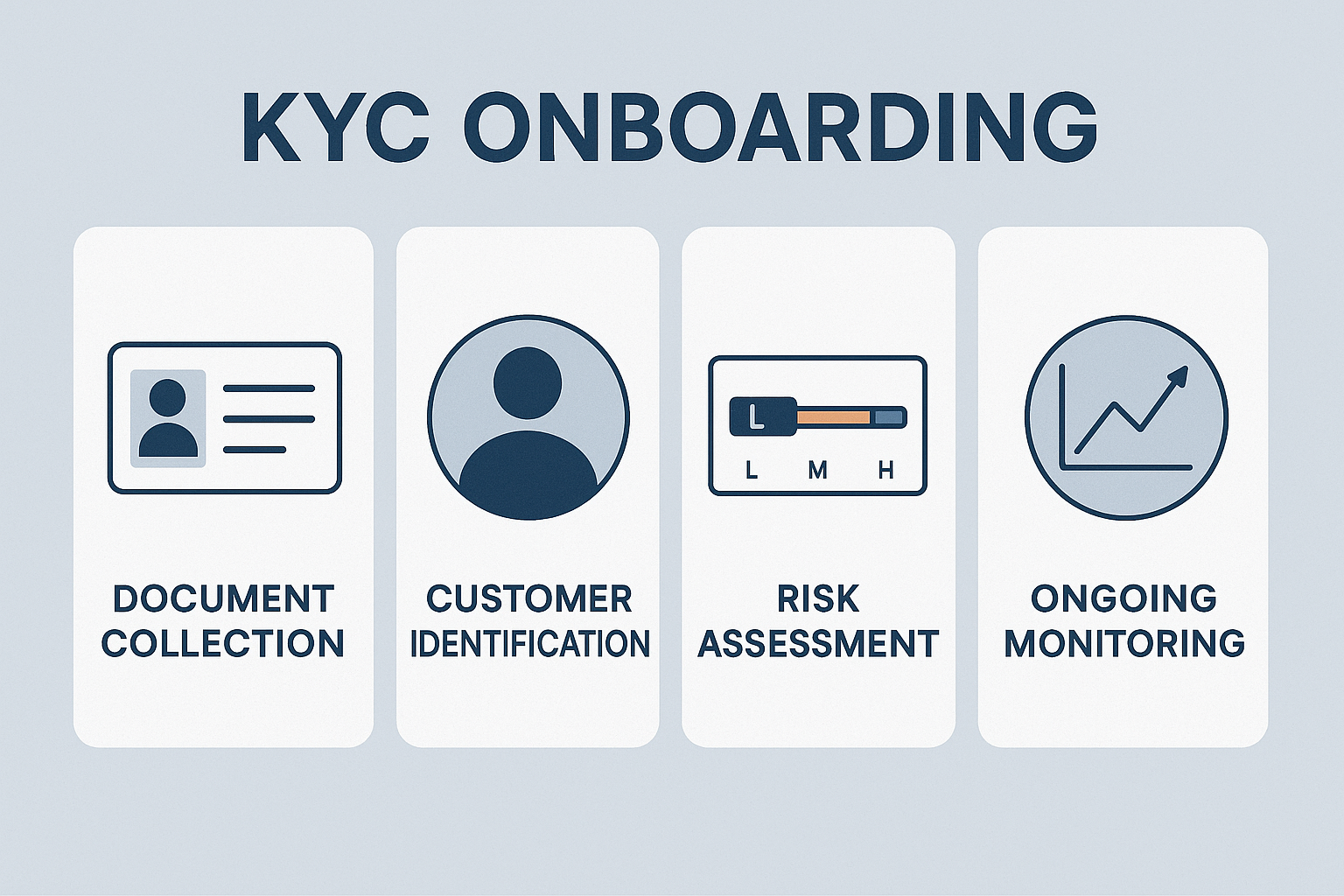

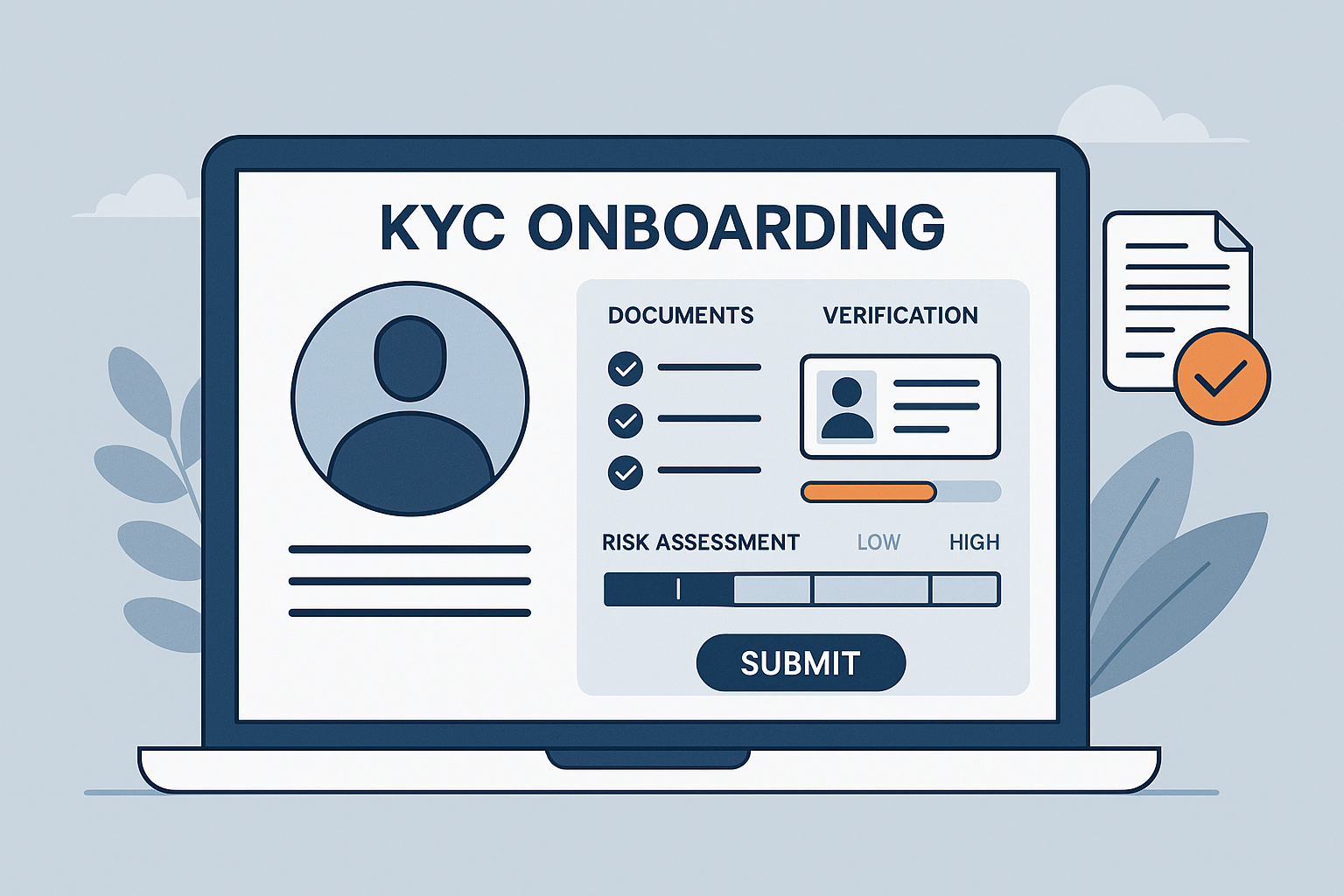

Core Elements of Effective KYC Onboarding

Customer Identification Program (CIP)

Collect official documents such as passports, business registration numbers, and bank statements. Automating this step minimizes manual errors.

Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD)

CDD verifies identity and assesses risk levels. High-risk merchants require EDD, which involves deeper scrutiny and continuous transaction monitoring.

Ongoing Monitoring and Risk Assessment

KYC doesn’t stop after onboarding. Providers must monitor accounts for suspicious activity and update records as necessary.

Best Practices for Merchant Account Providers

Automate the KYC Process with AI and ML

Automation improves speed and accuracy while reducing manual errors. Machine learning algorithms can identify document anomalies and flag high-risk profiles in real time.

Maintain a Risk-Based Approach to Onboarding

Not all merchants pose the same risk. Apply tiered verification protocols depending on business type, transaction volume, and geography.

Ensure Transparent and Secure Document Collection

Use encrypted platforms for document uploads to ensure data privacy and GDPR compliance.

Regularly Update and Train Compliance Teams

UKYC regulations evolve frequently. Continuous staff training ensures everyone understands new standards and technologies.

Integrate KYC with AML and Fraud Detection Systems

A unified compliance ecosystem allows better tracking of merchant behavior and early detection of fraudulent activities.

How Technology is Transforming KYC in 2025

From biometric authentication to blockchain-based identity verification, technology is revolutionizing how providers conduct KYC.

eKYC (electronic KYC) eliminates paper-based processes, reducing onboarding time.

Blockchain enhances data integrity by providing immutable verification records.

These tools make compliance seamless while offering a frictionless experience for legitimate merchants.

High-risk merchants

| Impact: Increases fraud exposure |

| Solution: Use enhanced due diligence (EDD) |

False positives

| Impact: Delays onboarding |

| Solution: Fine-tune screening tools |

Regulatory changes

| Impact: Compliance risk |

| Solution: Regularly update KYC policies |

Poor UX

| Impact: Merchant drop-offs |

| Solution: Simplify onboarding workflows |

Key Metrics for Measuring KYC Onboarding Success

Verification Time: Average time to verify merchant documents.

Accuracy Rate: Ratio of correct verifications to total checks.

Drop-off Rate: Percentage of merchants abandoning onboarding.

Audit Scores: Indicators of compliance health.

Case Study: Streamlining KYC for Fintech Merchant Accounts

A fintech company previously spent 72 hours onboarding each merchant. After integrating automated KYC tools and biometric verification, verification time dropped to under 10 minutes, with compliance accuracy increasing by 35%. This not only improved operational efficiency but also enhanced trust among merchants and regulators.

FAQs about KYC Onboarding for Merchant Account Providers

Conclusion: Future-Proofing KYC Onboarding in 2025 and Beyond

In 2025, merchant account providers face both challenges and opportunities in KYC compliance. By embracing automation, risk-based due diligence, and digital identity verification, they can streamline operations while staying compliant. The future belongs to providers who treat KYC not as a burden — but as a strategic advantage for security, trust, and growth.